2,28

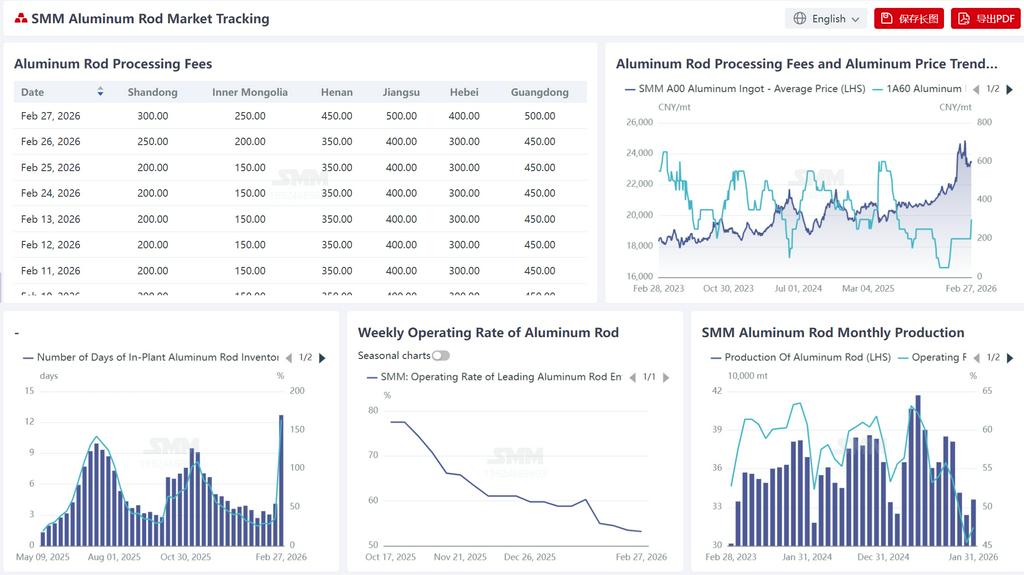

Selon SMM, au 27 février 2026, les stocks des usines de barres d'aluminium en Chine s'élevaient à 12,7 jours, soit une augmentation de 8,6 jours par rapport à la période avant les vacances. En termes de ratio de stock, le ratio de stock en usine pour les usines de barres d'aluminium en Chine était de 163,8 %, indiquant que la pression du stockage en usine n'est pas légère.

Après les vacances, le centre des prix de l'aluminium a rebondi par rapport aux niveaux d'avant les vacances, mais le sentiment du marché n'était pas entièrement rétabli au début de la nouvelle année. Les offres de frais de transformation montraient une différenciation régionale, mais maintenaient globalement des prix fermes. Concernant les différents frais de transformation, au 28 février 2026, les frais de transformation pour les barres d'aluminium dans la région du Jiangsu étaient cotés entre 450 et 550 yuans/tonne, dans le Hebei entre 350 et 450 yuans/tonne, et dans le Sud de la Chine entre 350 et 500 yuans/tonne. Revenons aux frais de transformation pour les barres d'aluminium dans différentes régions, la région du Shandong était cotée entre 250 et 350 yuans/tonne, la Mongolie-Intérieure entre 200 et 300 yuans/tonne, et le Henan entre 400 et 450 yuans/tonne. Malgré la tendance marquée de l'accumulation des stocks de barres d'aluminium due aux effets saisonniers, la reprise de la consommation en aval était meilleure que prévu avant les vacances, avec des attentes claires pour les livraisons de réseau électrique en mars. La demande des usines de câbles et fils en aval a fortement rebondi, ce qui favorisera davantage la reprise du sentiment commercial sur le marché des barres d'aluminium. L'espace pour l'accumulation de stocks est relativement limité, et il est attendu que les frais de transformation pour les barres d'aluminium en mars évoluent de manière stable et légèrement forte.

La première semaine après les vacances, le taux d'activité hebdomadaire de l'industrie chinoise des câbles et fils en aluminium a rebondi à 57 %, soit une augmentation de 4 points de pourcentage en glissement mensuel, nettement supérieur au plus bas niveau d'avant les vacances de 53 %. Le facteur moteur central était les commandes continues du réseau électrique après les vacances, correspondant et activant les commandes d'entreprises, avec une reprise du travail des entreprises légèrement supérieure aux attentes. Le point bas saisonnier actuel de l'industrie est passé, et les attentes de prise de marchandises après les vacances sont positives. La production en aval devrait atteindre un plancher et se redresser, passant progressivement de la basse saison à la haute saison. À court terme, il convient de prêter une attention particulière à la réalisation des attentes de commandes de State Grid pour mars et à l'avancement de la correspondance des anciennes commandes. Si la durabilité des commandes montre de l'optimisme, le taux d'exploitation en aval présentera une tendance favorable. L'accent sera mis sur le rythme de mise en œuvre des commandes du réseau électrique et la vigueur de la reprise de la demande finale. On s'attend à ce que le taux d'exploitation de l'industrie du fil et du câble en aluminium rebondisse à 59 % la semaine prochaine.